How I Turned My Home Office Into a Profit Hub—Remote Work Returns, Reimagined

Working from home used to mean saving on gas and skipping office small talk. But over time, I realized my remote setup wasn’t just cutting costs—it could actually boost my earnings. I started treating my work-from-home life like a financial strategy, not just a convenience. What if your laptop, Wi-Fi, and quiet morning hours weren’t just tools for your job, but assets for growing wealth? That shift in mindset changed everything. The truth is, remote work offers more than flexibility—it opens a path to smarter income generation, better time use, and long-term financial control. When approached with intention, your home office can evolve from a simple workspace into a profit-generating hub.

The Hidden Financial Reality of Remote Work

Remote work is often celebrated for its convenience—no rush-hour traffic, no rigid dress codes, and more time with family. But beneath the surface lies a powerful financial opportunity that many overlook. The real value of working from home isn’t just in the hours saved or the coffee not bought; it’s in the ability to reconfigure those savings into active wealth-building strategies. Traditional employment models reward time spent, not results achieved. In contrast, remote work—when managed strategically—allows individuals to decouple effort from compensation in new and profitable ways.

Consider this: the average American commuter spends nearly 30 minutes each way traveling to work, totaling over 200 hours per year. That’s the equivalent of five full workweeks reclaimed. For remote workers, these hours don’t have to vanish into passive recovery or household chores—they can be reinvested into income-generating activities. This is what economists call "time arbitrage": using low-cost personal time to create higher-value financial outcomes. A teacher might use that time to develop an online course. A project manager could consult part-time for startups. An accountant might automate tax templates and sell them digitally. These are not pipe dreams—they’re realistic extensions of existing skills made possible by remote flexibility.

Moreover, remote work shifts the balance of financial control back to the individual. Without the constant visibility of office culture, performance is often judged more on output than presence. This creates space to experiment with new income models without immediate scrutiny. Workers can test side projects, refine offerings, and scale gradually—all while maintaining their primary income stream. The key is recognizing that remote work isn’t just a job format; it’s a financial platform. When viewed through this lens, every decision—from internet speed to desk placement—takes on new economic significance.

Yet, many remote workers fail to capitalize on this potential. They replicate the 9-to-5 structure at home, logging the same hours without reaping additional rewards. The difference between average and exceptional outcomes lies in mindset. Those who thrive financially don’t just work remotely—they treat their setup as a business operation. They track time not just for productivity, but for profitability. They assess tools not just for comfort, but for return on investment. This subtle but critical shift transforms remote work from a cost-saving arrangement into a strategic advantage.

Turning Time Gains Into Financial Gains

The most tangible benefit of remote work is time. Without a daily commute, meetings often start later, and personal schedules become more fluid. But time alone is not wealth. It becomes valuable only when allocated with intention. Many remote workers fall into the trap of either overworking—blurring the lines between home and office—or underutilizing their freedom, filling reclaimed hours with passive entertainment. The financially savvy remote worker, however, treats time as a currency to be invested wisely.

One of the most effective ways to convert time into financial gain is through skill monetization. The digital economy rewards specialized knowledge, and remote workers are uniquely positioned to develop and sell it. For example, a marketing professional might spend two hours a week learning SEO analytics, then apply that knowledge to freelance for small businesses. A software developer could create reusable code snippets and license them on platforms designed for developers. These activities don’t require quitting a day job—they simply require consistent, focused effort during otherwise idle moments.

Another high-return use of time is passive income development. Unlike active work, which trades hours for dollars, passive income continues to generate returns with minimal ongoing effort. Remote workers can leverage their quiet mornings or lunch breaks to build digital products—e-books, templates, or online courses—that sell repeatedly. A graphic designer might create a set of social media templates. A financial analyst could develop a budgeting spreadsheet with automated formulas. Once created, these assets can generate income for months or even years with little maintenance.

Time can also be used to improve financial literacy. Understanding personal finance—budgeting, investing, tax optimization—is one of the highest-leverage skills a remote worker can develop. An hour spent learning about index funds or retirement accounts may seem less urgent than answering emails, but its long-term impact far exceeds short-term tasks. Many remote workers who build wealth consistently allocate time each week to financial education, treating it as non-negotiable as any work meeting.

Of course, time gains can be eroded by inefficiencies. Common pitfalls include working longer hours without higher pay, falling into digital distractions, or failing to set boundaries. Without a structured approach, the flexibility of remote work can lead to burnout rather than benefit. The solution is time blocking—scheduling specific hours for primary work, skill development, and financial management. By treating time as a finite resource, remote workers can ensure that every hour contributes to either income, growth, or rest—never wasted.

Home as a Strategic Financial Base

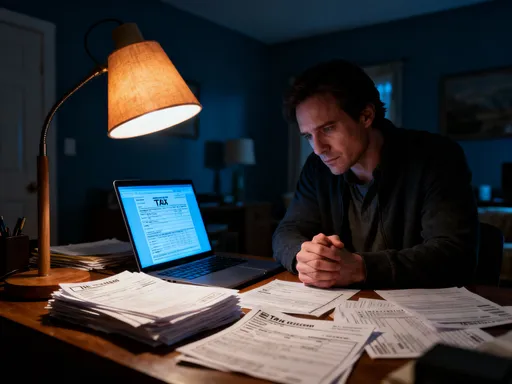

The home office is more than a corner of the living room with a laptop. When optimized, it becomes a financial asset with multiple layers of value. The first and most direct benefit is the home office tax deduction. In many countries, self-employed individuals and eligible remote workers can deduct a portion of rent, utilities, internet, and even home improvements related to their workspace. This isn’t about aggressive tax avoidance—it’s about claiming legitimate expenses that support income generation. A well-documented home office can reduce taxable income, effectively increasing take-home pay.

Beyond taxes, the physical setup of a home office influences financial efficiency. High-speed internet, reliable power, and noise control aren’t just comfort features—they’re productivity enablers. A stable connection allows for seamless video calls, faster uploads, and access to global freelance markets. A quiet environment enables deep work, where high-value tasks are completed in less time. These factors compound: better conditions lead to better output, which leads to higher earnings or faster project completion, freeing up even more time for financial growth.

Some remote workers take this further by transforming their space into a revenue-generating environment. A spare room with good lighting and acoustics can become a content creation studio for YouTube, podcasts, or online teaching. Others sublet part of their home as a co-working space during off-hours, generating rental income without disrupting their own schedule. These models work best when aligned with existing routines—using the same equipment for both primary and secondary income streams.

However, there is a risk of lifestyle inflation. It’s easy to justify expensive ergonomic chairs, standing desks, or smart lighting as "work necessities." While comfort matters, not every upgrade delivers a financial return. The key is cost-benefit analysis: will this purchase increase productivity enough to justify its cost? A $1,200 chair may feel luxurious, but if it doesn’t significantly improve focus or health, it’s a luxury, not an investment. Smart remote workers prioritize tools that deliver measurable returns—like a second monitor that speeds up workflow or noise-canceling headphones that reduce meeting fatigue.

The most strategic approach treats the entire home as a financial ecosystem. Energy-efficient lighting lowers utility bills. A dedicated workspace reduces distractions, improving work quality. Even furniture placement can influence focus and efficiency. When every element serves a dual purpose—function and financial benefit—the home becomes more than a place to live. It becomes a foundation for sustained wealth creation.

Income Layering: Beyond the Primary Paycheck

One of the most powerful financial strategies for remote workers is income layering—the practice of building multiple revenue streams that complement, rather than compete with, a primary job. Unlike traditional employment, where side work might be restricted or frowned upon, remote roles often offer the autonomy and schedule predictability needed to pursue additional income without conflict.

The foundation of successful income layering is alignment. The best side ventures leverage existing skills, tools, and routines. A writer might offer copyediting services in the evenings. A data analyst could create dashboards for small businesses on weekends. These activities don’t require reinventing the wheel—they simply extend professional expertise into new markets. Because the infrastructure is already in place—a computer, software, internet connection—the marginal cost of adding a second income stream is low.

Digital products are particularly effective for layering. Once created, they can be sold repeatedly with minimal effort. A teacher might record a series of video lessons and sell them on an education platform. A fitness coach could design a downloadable workout plan. These products scale well: one hour of creation can lead to hundreds of dollars in sales over time. Unlike hourly consulting, which trades time for money directly, digital products decouple effort from income, allowing remote workers to earn while they sleep.

Another viable path is micro-investing during downtime. Many remote workers have short breaks between meetings or tasks. Instead of scrolling social media, they can use that time to review portfolios, rebalance investments, or research new opportunities. Apps that automate investing—such as those that round up purchases and invest the difference—make it easy to grow wealth incrementally. Over time, these small actions compound into significant returns.

It’s important to avoid get-rich-quick schemes. True income layering is not about gambling on crypto or chasing viral trends. It’s about consistent, low-risk efforts that build over time. The goal is not to replace the primary income overnight, but to create a buffer—a second, third, or even fourth stream that increases financial resilience. When one source slows, others can compensate. This diversification reduces stress and increases long-term security.

Risk Control in a Decentralized Work World

With the freedom of remote work comes increased financial responsibility. Unlike traditional office jobs, where career progression is often structured and benefits are standardized, remote work requires individuals to manage their own safety nets. There is no automatic mentorship, no HR department to advocate for raises, and no guaranteed path to promotion. This autonomy is empowering—but it also demands proactive risk management.

The first line of defense is an emergency fund. Financial advisors often recommend three to six months of living expenses saved in liquid accounts. For remote workers, this cushion is even more critical. Income from side projects can fluctuate. Contracts may end unexpectedly. Technology failures can disrupt work. Without a stable emergency fund, these events can lead to financial stress or debt. Building this fund should be a priority, even if contributions are small at first.

Diversification is another key strategy. Relying on a single employer or client is risky. The financially resilient remote worker spreads income across multiple sources—primary job, freelance work, digital products, and investments. This reduces dependence on any one stream and increases stability. If one project ends, others continue. If the job market shifts, diversified skills provide more options.

Career stagnation is a less obvious but real risk. Without office interactions, remote workers may miss informal learning opportunities or networking events. Over time, this can lead to skill obsolescence. The solution is intentional professional development. Setting aside time each month for learning—whether through online courses, industry webinars, or peer groups—acts as financial insurance. Updated skills increase marketability and open doors to higher-paying opportunities.

Digital security is also a form of risk control. Remote work depends on devices, accounts, and data. A single breach can disrupt income, damage reputation, or lead to financial loss. Using strong passwords, two-factor authentication, and secure networks is not optional—it’s essential. Backing up files regularly ensures that work is never lost to technical failure. These habits may seem minor, but they protect the very foundation of remote earnings.

Tech and Tools That Multiply Returns

Not every app or software subscription delivers value. In fact, many remote workers fall into the trap of "tool overload"—paying for multiple platforms that promise productivity but deliver confusion. The most effective tools are those that save time, reduce errors, and generate measurable financial returns.

Automation tools are among the highest-impact investments. Software that auto-schedules social media posts, sends invoice reminders, or categorizes expenses frees up hours each week. For example, a freelancer using automated invoicing can get paid faster and reduce late payments. A small business owner using accounting software can file taxes more accurately and claim more deductions. These tools don’t just improve efficiency—they directly affect the bottom line.

Investment platforms that simplify portfolio management are also valuable. Many remote workers lack the time to monitor markets constantly. Robo-advisors and automated rebalancing tools allow them to invest wisely without daily oversight. These platforms use algorithms to adjust allocations based on risk tolerance and goals, making investing more accessible and less emotional.

Productivity apps that track time and focus can reveal hidden inefficiencies. By analyzing how time is actually spent, remote workers can eliminate low-value tasks and double down on high-return activities. For instance, discovering that two hours a week are lost to unproductive meetings might prompt a renegotiation of calendar commitments. These insights lead to better decisions and stronger financial outcomes.

The key is to adopt tools selectively. Before subscribing, ask: Does this solve a real problem? Will it save time or money? Can I measure its impact? If the answer isn’t clear, it’s better to wait. The goal isn’t to have the most tools, but the right ones—those that deliver compound returns over time.

Building a Sustainable Remote Financial Future

True financial success in remote work isn’t about working more—it’s about working smarter. The most effective strategies are not dramatic overhauls, but consistent, compoundable actions. Tracking income streams, reviewing expenses, and adjusting goals monthly creates a feedback loop that drives progress. The remote worker who builds lasting wealth isn’t the one burning out at midnight, but the one who uses discipline, planning, and patience to grow value over time.

Mindset remains the foundation. Viewing the home office as a profit center changes how every decision is made. A Wi-Fi upgrade isn’t just convenience—it’s infrastructure. A course in financial planning isn’t just learning—it’s an investment. Even rest becomes strategic, preserving energy for high-leverage activities.

Ultimately, remote work offers a rare opportunity: the chance to align daily life with long-term financial goals. By treating time, space, and skills as assets, and by managing risk with care, remote workers can build a future that is not only flexible but financially secure. The home office, once seen as a temporary setup, can become the cornerstone of a sustainable, profitable life.